Fixed Deposits (FDs) remain the bedrock of Indian household savings. Despite the rise of mutual funds, stock markets, and crypto, the humble FD continues to attract crores of investors - and for very good reason.

What is a Fixed Deposit (FD)?

An FD is simple: you deposit a lump sum with a bank or financial institution for a fixed tenure, and the bank pays you a guaranteed rate of interest.

No market drama. No sudden losses. Just predictable, compounding growth.

But here's what most people don't realise: not all FDs are created equal.

The type of FD you choose, the bank you pick, the tenure you select, and the payout option you opt for can collectively make a difference of ₹50,000-₹1,00,000 or more on a ₹10 lakh investment over three years.

As of April 2026, FD interest rates range from about 2.5% to 8.30% per annum, depending on tenure and bank type. Small Finance Banks are offering 7% to 8.30%, making them the top choice for investors prioritising higher returns, while public sector banks and large private banks typically provide 6% to 7%.

This guide helps you make all those choices wisely.

10 Types of Fixed Deposits in India 2026

India's banking system offers a surprisingly rich menu of FD products tailored to different financial goals, tax situations, and investor profiles.

Here's a comprehensive breakdown of every type you need to know.

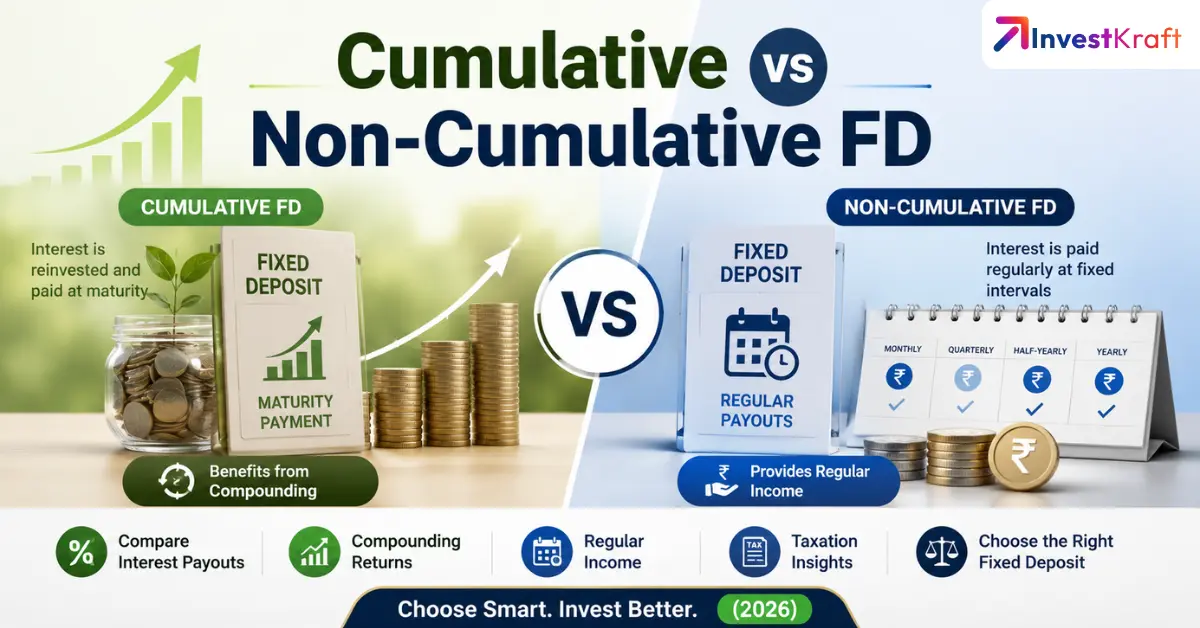

1. Cumulative FD (Growth FD)

In a cumulative FD, the interest earned is not paid out periodically - it is compounded quarterly and reinvested into the principal. You receive both the principal and the total accumulated interest only at maturity.

In cumulative fixed deposits, your earned interest compounds, and the total interest is paid at maturity. This type of deposit works best when you can maintain the investment duration and withdraw after maturity. It is suitable for goal-based investments like kids' education or maintaining an emergency fund.

This is the best type for long-term wealth creation because compound interest works in your favour.

A ₹5 lakh FD at 8% for 5 years grows to roughly ₹7.4 lakh on a cumulative basis - noticeably more than a non-cumulative FD of the same rate.

Best for: Wealth building, long-term goals

2. Non-Cumulative FD (Income FD)

Non-Cumulative FD, the interest is paid out at regular intervals - monthly, quarterly, half-yearly, or annually. The principal remains locked in. This is perfect for retirees or anyone who needs a regular income stream from their savings.

Monthly payout FDs typically pay a slightly lower effective interest rate because the bank pays you early. Choose quarterly or annual payouts where possible to maximise returns.

Best for: Retirees, senior citizens, regular income needs

Many banks, under their special schemes and for specific tenures, offer an additional interest rate of 0.20%-0.50% over and above their senior citizen FD rates.

Furthermore, some banks also offer additional interest rates to super senior citizens (aged 80 years and above). For instance, Indian Bank offers an additional interest rate of 0.75% p.a. to super senior citizens for tenures of up to 5 years.

Example: Suryoday Small Finance Bank offers interest rates up to 8.25% for senior citizens versus 8.10% for general citizens (as of April 2026). This differential compounds meaningfully over 3-5 years.

Tax-saving Fixed Deposit: Available only to resident individuals and HUFs, this FD allows a tax deduction of up to ₹1.5 lakh under Section 80C and has a 5-year lock-in period.

Premature withdrawal is not permitted. Interest earned is taxable as per your income slab. But the upfront tax saving can significantly improve your effective returns - especially if you're in the 20% or 30% tax bracket.

Best for: Salaried taxpayers, HUFs

5. Non-Callable FD

Non-callable FD is opposite to callable fixed deposits in the sense that the depositors can withdraw their investments only at maturity. The interest rates offered on non-callable FDs are usually higher than the interest rates offered on callable FDs. Typically, 0.15%-0.30% more for the same tenure. These are ideal for money you are 100% sure you won't need before maturity.

Best for: Investors with surplus funds they can lock away

6. Flexi FD (Sweep-in FD)

Flexi FD allows depositors to link their FDs with their savings or current account. In case of a fund deficit in the linked savings account, the linked deposit amount can be partially broken, and the remaining deposit amount will continue to earn the FD interest rate.

You earn FD-level interest on your idle savings while retaining complete liquidity. Major banks like HDFC, Axis, and ICICI offer this feature.

Best for: Salaried professionals with fluctuating cash flows

7. Floating Rate FD

Floating Rate Fixed Deposit has its interest rate linked to a reference rate, such as the RBI's Repo Rate or T-Bill Rate, meaning returns vary based on changes in the reference rate.

In a rising rate environment, these FDs can outperform standard ones. In a declining rate cycle - like the current RBI easing phase - they underperform.

Best for: Investors who believe interest rates will rise

8. Corporate FD (Company FD / NBFC FD)

Corporate FD, offered by Non-Banking Financial Companies (NBFCs) like Bajaj Finance, Muthoot Capital, and Shriram Finance, corporate FDs often provide 0.5%-2% higher rates than bank FDs.

Critical Note: NBFCs (Non-Banking Financial Companies) are not covered under DICGC. This insurance applies only to RBI-registered banks. So, money in NBFCs, chit funds, or finance companies don't have this protection. Always check the credit rating - look for CRISIL or ICRA AAA/AA+ ratings before investing.

Best for: Higher-yield seekers who understand credit risk

NRE (Non-Resident External) Deposits are for Non-Resident Indians and Persons of Indian Origin who wish to deposit their foreign earnings. NRO (Non-Resident Ordinary) Deposit is for NRIs and PIOs who want to deposit their income earned through Indian sources. FCNR (Foreign Currency Non-Resident) Deposit is for NRI and PIO customers who want to deposit their funds generated/earned overseas.

NRE FD interest is completely tax-free in India and fully repatriable - making it particularly attractive for the Indian diaspora.

Best for: Non-Resident Indians

10. Small Finance Bank FD

Small Finance Banks are noted for offering the market's highest FD interest rates. This trend is expected to continue in 2026, with SFBs leading the way, with several offering well over 7% to the general public and approximately 8% or more to seniors.

They are fully regulated by the RBI and covered by DICGC insurance up to ₹5 lakh per depositor per bank. More on SFBs in a dedicated section below.

Best for: Yield-maximisers comfortable with regulated SFBs

Post Office FD - The Government-Backed Alternative

For investors who want sovereign-backed safety beyond the ₹5 lakh DICGC limit, the Post Office Time Deposit is an excellent option. Unlike bank FDs, Post Office FDs carry a full Government of India guarantee - meaning there is no practical upper limit on what is safe.

Current Post Office FD Rates (June 2026):

Tenure

Interest Rate (p.a.)

Tax Benefit

1 Year

6.90%

No

2 Years

7.00%

No

3 Years

7.10%

No

5 Years

7.50%

Yes - Section 80C

The 5-year Post Office FD at 7.50% with Section 80C benefit is particularly attractive for taxpayers in the higher brackets. Post offices also offer accessibility through 1,60,000+ outlets nationwide, making them ideal for investors in smaller towns and rural areas.

FD Interest Rates 2026 - Bank-wise Comparison

Here is a comprehensive look at the latest FD interest rates as of April 2026, across all major bank categories. Always verify current rates on the official bank website before investing, as rates change frequently.

Public Sector Banks

State Bank of India (SBI): FD interest rates from 3.05% to 6.40% p.a. for the general public and 3.55% to 7.05% for senior citizens. The highest interest rate of 6.40% for the general public is provided on the two-year fixed deposit.

Punjab National Bank (PNB): FD interest rates of 3% to 6.60% p.a. to the general public and 3.50% to 7.10% p.a. to senior citizens. The highest interest rates are provided on FDs of 444 days tenure.

Private Sector Banks

HDFC Bank: FD rates in the range of 6.25% to 6.50% for key tenures. The highest rate of 6.50% is available for deposits between 3 years and 4 years 7 months. The bank maintains a consistent rate structure across tenures, making it suitable for investors seeking stability.

ICICI Bank: Competitive, especially in the 3-5 year bucket, where it offers up to 6.50%. Its uniformity across longer tenures makes it attractive for investors locking in rates for the medium to long term. Senior citizens earn up to 7.10%.

Axis Bank: FD interest rates from 3% to 6.45% p.a. for the general public and from 3.50% to 7.20% p.a. for senior citizens across tenures of 7 days to 10 years. The rates are applicable from April 7, 2026.

Kotak Mahindra Bank: Rates of up to 6.80% for general depositors, with particularly competitive rates in the 2-3 year bucket. Senior citizens earn up to 7.30%.

Bandhan Bank: Interest rates from 2.95% to 7.25% to the general public and 3.70% to 7.75% to senior citizens. The highest rates are provided on two-year fixed deposits. The rates are applicable from March 5, 2026.

RBL Bank: Leads among private banks at 7.20% for general depositors.

Small Finance Banks (Highest Rates)

Among all banking categories, Small Finance Banks are currently leading the interest rate spectrum. Suryoday Small Finance Bank tops the chart with FD rates of 7.90%, followed by Jana Small Finance Bank at 7.77% and Utkarsh Small Finance Bank at 7.25%. Ujjivan SFB offers 7.20%, while AU and Equitas SFBs are at 7.00%.

For maximum rates, April 2026 data shows:

Suryoday SFB: Up to 8.10% (general), 8.25% (senior citizen)

ESAF SFB: Up to 8.00% (general), 8.50% (senior citizen)

Shivalik SFB: Up to 7.80% (general), 8.30% (senior citizen)

Jana SFB: Up to 7.77% (general)

Ujjivan SFB: Up to 7.20% (general)

Utkarsh SFB: Up to 7.25% (general)

AU SFB: Up to 7.00% (general)

NBFCs / Corporate FDs

Non-Banking Financial Companies continue to offer competitive FD rates, often surpassing traditional banks across select tenures. Muthoot Capital Services offers up to 8.50% for 3- and 5-year tenures. Shriram Finance offers 7.60%. PNB Housing Finance and Bajaj Finance provide rates up to 7.10%-7.30%.

Currently, the highest rate available for senior citizens is up to 9.35% p.a. from Muthoot Capital.

Remember: NBFC FDs are NOT covered by DICGC insurance.

One of the biggest concerns for FD investors - especially those considering Small Finance Banks - is whether their money is safe if the bank fails.

What is DICGC?

DICGC stands for Deposit Insurance and Credit Guarantee Corporation, which is a wholly-owned subsidiary of the Reserve Bank of India that provides depositors security of up to ₹5 lakh in case a bank collapses or is placed under moratorium.

What does it cover?

Coverage limit is ₹5 lakhs per depositor, per bank. It covers all commercial banks, including foreign banks operating in India, local area banks, and regional rural banks. It includes savings, fixed, current, and recurring deposits. This insurance is automatic and doesn't require any separate registration.

How does the ₹5 lakh limit work?

Every depositor is insured for up to ₹5,00,000 per bank. It includes the sum of principal and interest across all accounts - savings, FDs, current accounts, and recurring deposits - within the same bank. If you have deposits in multiple banks, the ₹5 lakh limit applies separately to each bank.

What is NOT covered?

NBFCs (Non-Banking Financial Companies) are not covered under DICGC. Money in NBFCs, chit funds, or finance companies doesn't have this protection. DICGC does not cover post office deposits either - post offices offer their own separate safety net.

What about the accrued interest trap?

Only ₹5 lakh receives DICGC protection regardless of interest accrual. Amounts exceeding this limit remain uninsured and at risk during bank failures. Factor in projected interest when deciding how much to put in one bank - a ₹4.5 lakh FD at 8% over 2 years will cross ₹5 lakh before maturity.

When does DICGC pay?

As per the DICGC (Amendment) Act, 2021, DICGC must complete payment within 90 days of receiving the bank's data. Depositors are not required to file any claim with the bank - the system is centralised and automated.

Future Developments

The Ministry of Finance is considering hiking deposit insurance in India provided by DICGC from ₹5 lakh to ₹8-12 lakh. If implemented, this would significantly expand the safety net for depositors.

Smart Strategy

Spreading fixed deposits across multiple banks dramatically increases your insured amount. A smarter approach is to split deposits across multiple banks, keeping each deposit within the insurance limit. This simple strategy protects your entire FD portfolio without reducing safety.

What Decides FD Rates - And Why Do They Rise or Fall?

FD rates don't exist in a vacuum. They are shaped by a complex interplay of macroeconomic forces and each bank's financial position.

The RBI Repo Rate - the master switch: The Repo Rate is the most important driver of FD rates. When the RBI raises repo rates, banks also increase FD rates and vice versa. As of April 2026, following rate cuts in 2025, the repo rate stands at 5.25%, which has put mild downward pressure on FD rates across major banks.

Inflation: When inflation rises, the RBI raises rates to cool the economy, which pushes FD rates up. During periods of low inflation, the RBI eases rates, pulling FD returns down. Always think of your real return as: FD rate minus inflation rate.

Liquidity in the Banking System: Economic conditions such as inflation, liquidity in the banking industry, and GDP growth impact FD rates. When the banking system is flush with liquidity and deposit growth outpaces credit demand, banks have no urgency to attract deposits - so rates drift lower.

Credit Demand and Economic Growth: A growing economy fuels demand for loans. High credit demand forces banks to mobilise more deposits, pushing FD rates up. In an economic slowdown, loan demand falls, and FD rates trend lower.

Each Bank's Individual Position: A bank aggressively growing its loan book will offer higher FD rates. A bank sitting on excess liquidity will offer lower rates. This is why rates differ by 50-100 basis points even between banks of similar size.

Why Do Small Finance Banks Offer Higher FD Rates?

This is the most common question from FD investors - and the answer is rooted in both economics and regulation.

They Depend Heavily on Retail Deposits: Large banks like SBI and HDFC have access to diverse funding sources - current accounts, government deposits, bonds, and inter-bank borrowing. Small Finance Banks have limited funding sources and rely heavily on retail deposits, which translates into better returns for investors. To attract those deposits, they offer more competitive rates.

They Serve Higher-risk Borrowers: Small Finance Banks primarily focus on financial inclusion and serving underserved segments such as small entrepreneurs, low-income households, and micro-businesses. Their lending is largely to small businesses and higher-risk segments. To compensate, they provide depositors with more attractive interest rates.

RBI Mandates Shape their Costs: The RBI mandates a 15% Capital Adequacy Ratio for SFBs - higher than commercial banks - since SFBs lend to riskier borrowers. This oversight helps ensure financial discipline and depositor protection. But it also constrains their financing, increasing their reliance on retail deposits.

They're Newer and need to compete: Small Finance Banks often maintain higher rates even when the RBI cuts rates, as they depend more heavily on deposit mobilisation. Large banks adjust rates more quickly to policy changes.

The Safety Picture: Small Finance Banks are still regulated by the RBI and covered by the same deposit insurance system, which means the higher rate does not automatically imply higher risk for insured deposits within the ₹5 lakh limit. As Business Standard pointed out in February 2026, the real risk is not choosing a smaller bank - it's keeping too much money in one bank.

Best Apps to Invest in Fixed Deposits (FDs) in 2026

Gone are the days when opening an FD required a branch visit. Several well-regulated platforms now let you compare, invest, and manage FDs from multiple banks in one place.

Stable Money: Bangalore-based SEBI-registered Research Analyst (INH000024912) and AMFI-registered mutual fund distributor. Stable Money lets you invest in FDs from SFBs and banks - including Shivalik SFB, Unity SFB, Suryoday SFB, and more - digitally, with a single KYC. Trusted by over 30 lakh customers. It also offers FD rate comparison across banks and is a useful one-stop destination for retail FD investors.

Paisabazaar: India's largest financial marketplaces, lets you compare FD rates from dozens of banks and NBFCs and apply online. Strong for comparison before you decide where to invest.

GoldenPi: Known primarily for bonds, but also offers access to SFB FDs and NBFC deposits. Good if you want to combine FD investing with other fixed-income instruments like bonds and debentures.

ET Money / BankBazaar: Offer FD rate comparison tools across a wide range of banks and NBFCs. Helpful for identifying the best tenure-rate combination before investing directly on a bank's own platform.

Direct bank apps remain the safest and most direct route for FDs with your own bank - HDFC, SBI, ICICI, Axis, and most SFBs now offer full-featured mobile apps with instant FD booking.

Note: Always verify that any third-party platform you use is appropriately registered. The FD contract remains between you and the bank; the platform simply facilitates. DICGC insurance applies to the underlying bank deposit regardless of the platform used.

Proven Strategies to Maximise FD Returns

Beyond just picking the highest rate, there are several smart strategies that can meaningfully boost your effective returns.

Choose cumulative FDs for long-term goals: If you don't need regular income, always choose the cumulative option. Compounding - interest earning interest every quarter - creates a meaningful premium over non-cumulative FDs of the same rate, especially over 3-5 year tenures.

Build an FD ladder: Don't put everything into one tenure. Split your investment across multiple tenures - say 1 year, 2 years, and 3 years. As each FD matures, you reinvest at the prevailing rate, averaging out interest rate risk over time and maintaining regular liquidity without breaking a long-term FD prematurely.

Spread across multiple banks to maximise DICGC coverage: Instead of parking ₹20 lakh in one bank, spread it across four or five banks - a mix of private banks and SFBs - keeping each bank's total (including projected interest) below ₹5 lakh. You get maximum DICGC coverage and can capture higher SFB rates on some tranches.

Target peak-yield tenures: Banks don't offer their best rates uniformly across all tenures. There's often a sweet spot - like 15 months, 444 days, or 2-3 years - where they offer peak rates. Always check the full rate chart and invest at the tenure that maximises returns.

Lock in now if rates are declining: In the current RBI rate-cutting cycle, longer-term FDs protect you from future rate drops. If you lock in a 3-5 year FD at 8%+ at an SFB today, you'll continue earning that rate even if the bank drops rates for new deposits next quarter.

Senior citizens: Always use the differential. The 0.50%-0.75% additional rate may seem small, but on ₹10 lakh over 5 years, it can add ₹30,000-₹45,000 in extra interest. Always opt for the senior citizen FD if you qualify.

Use Tax-Saving FDs wisely: If you're in the 30% tax slab and haven't exhausted your ₹1.5 lakh Section 80C limit, a Tax-Saving FD saves you ₹45,000+ in tax upfront. The effective post-tax return is superior to a regular FD at the same nominal rate for high-bracket taxpayers.

Take a loan against an FD rather than breaking it: Most banks offer loans against FDs at interest rates just 1-2% above the FD rate. If you face urgent cash needs, this preserves your interest accrual and avoids premature withdrawal penalties - almost always the smarter move.

Frequently Asked Questions

Which bank is best for a Fixed Deposit in 2026?

The best bank depends on your priorities. For maximum returns, Suryoday Small Finance Bank (up to 8.10% p.a.) leads. For a balance of returns and brand safety, Bandhan Bank (7.25%) or RBL Bank (7.20%) are strong private bank options. For those who prefer PSU safety, SBI or PNB are solid choices. For a large corpus above ₹5 lakh, spread across multiple banks, consider Post Office FDs for full sovereign safety.

All bank FD interest rates in 2026 - where do I check?

Always check directly on the official bank website: sbi.co.in, hdfcbank.com, icicibank.com, axisbank.com, etc. Rates change frequently - sometimes monthly - so any third-party comparison should be treated as a starting point, not the final word. Comparison platforms like Stable Money, Paisabazaar, and BankBazaar also maintain reasonably updated rate tables.

Which bank is best for a Fixed Deposit for 1 year?

For a 1-year tenure, ESAF SFB (up to 8.00%), Shivalik SFB (up to 7.80%), and Jana SFB (up to 7.77%) offer the highest rates among DICGC-covered institutions. Among large private banks, Bandhan Bank and RBL Bank are the strongest options for 1-year deposits.

Which bank gives the highest interest on FD per month (monthly income)?

SFBs like Suryoday and ESAF still lead for monthly payout FDs, though the effective monthly rate is slightly lower than the cumulative rate. Among large private banks, Bandhan Bank, RBL Bank, and Yes Bank offer the highest monthly payout rates. Always compare the effective annual rate - not just the nominal rate - when choosing a monthly payout FD.

What is the DICGC insurance limit, and does it cover Small Finance Banks?

Under the DICGC (Amendment) Act, 2021, the maximum deposit insurance coverage was enhanced to ₹5 lakh per depositor per bank. Yes, this covers all RBI-regulated banks, including Small Finance Banks. NBFCs like Bajaj Finance and Muthoot Capital are NOT covered.

What is the Post Office FD interest rate in 2026?

As of April 2026, Post Office Time Deposit rates are 6.90% for 1 year, 7.00% for 2 years, 7.10% for 3 years, and 7.50% for 5 years (with Section 80C benefit). These carry a full Government of India guarantee. Source: indiapost.gov.in.

What are Muthoot Finance / Muthoot Capital FD rates?

Muthoot Capital Services offers up to 8.50% for general investors and up to 9.35% for senior citizens on 3- and 5-year tenures as of April 2026. However, being an NBFC, these FDs are NOT covered by DICGC insurance. Always check the latest credit rating from CRISIL or ICRA before investing. Source:muthootcapital.com.

Is FD interest taxable? How does TDS work?

Yes, FD interest is fully taxable as "Income from Other Sources" per your income tax slab. Banks deduct TDS at 10% when interest exceeds ₹40,000 annually (₹50,000 for senior citizens). You can avoid TDS by submitting Form 15G (general) or Form 15H (senior citizens) if your total income is below the taxable limit.

Senior citizens can also claim up to ₹50,000 exemption under Section 80TTB.

What is the difference between cumulative and non-cumulative FDs?

In a cumulative FD, interest is compounded quarterly and paid at maturity along with the principal - best for wealth accumulation. In a non-cumulative FD, interest is paid out at regular intervals (monthly, quarterly, or annually) - best for regular income. For the same rate and tenure, a cumulative FD always generates more total interest due to compounding.

Can I lose money in an FD?

For amounts up to ₹5 lakh per bank, DICGC insurance ensures you cannot lose money even if the bank fails. For amounts above ₹5 lakh in a single bank, there is a theoretical risk if the bank goes into liquidation, though this is historically very rare for RBI-regulated banks. For NBFC FDs, there is no DICGC cover, making it important to check credit ratings. Post Office FDs carry a full government guarantee with no upper limit on safety.

Sources

All FD rate data sourced from official bank websites. Always verify before investing, as rates change frequently.

This article is for informational purposes only and does not constitute financial advice. FD interest rates change frequently - always verify the latest rates on the respective bank's official website before investing. Consult a registered financial advisor for personalised guidance.

Author: Diwakar Kumar Singh

Diwakar Kumar Singh is a BFSI specialist and finance writer with over 7 years of hands-on experience in financial research, content creation, and analysis.

A Gold Medalist in MBA (Marketing) from IMT, he combines deep analytical skills with practical insights gained from evaluating companies, IPOs, unlisted shares, financial ratios, and investment opportunities. Diwakar has personally analysed hundreds of financial instruments and market scenarios, which he uses to break down complex topics into clear, actionable advice.

He has authored numerous in-depth finance articles, published multiple books internationally, and contributed to research publications. His work focuses on helping everyday investors and readers make better-informed financial decisions through well-researched, evidence-based explanations that are always grounded in real-world application rather than theory alone.